2026 Social Security Adjustments: 3.5% COLA Impact

Anúncios

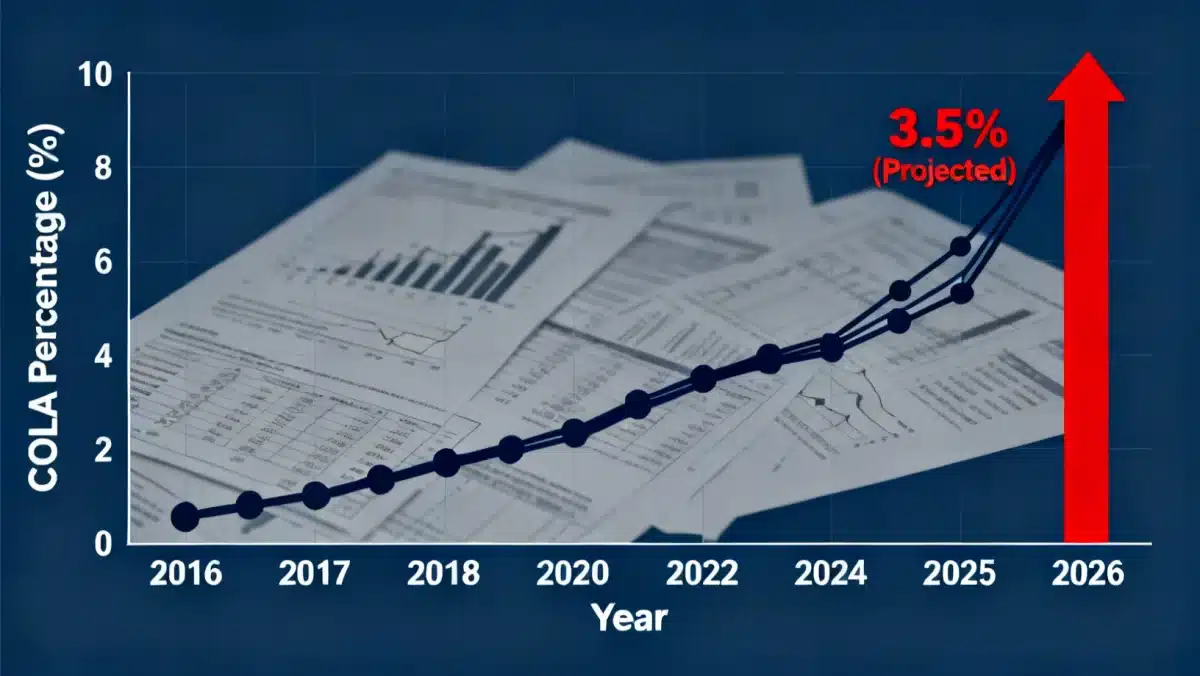

The projected 3.5% Cost-of-Living Adjustment (COLA) for 2026 Social Security benefits is poised to directly impact millions of Americans by increasing monthly payments, reflecting inflationary pressures and economic shifts.

For millions of Americans relying on their monthly payments, Understanding the 2026 Social Security Adjustments: What a 3.5% COLA Means for Your Benefits in the US is more than just financial jargon; it’s a critical insight into their future financial stability. This anticipated increase could significantly influence budgeting, spending power, and overall retirement planning. Let’s delve into what this adjustment truly entails.

Anúncios

Understanding the Cost-of-Living Adjustment (COLA)

The Cost-of-Living Adjustment (COLA) is a crucial mechanism designed to ensure that Social Security benefits retain their purchasing power in the face of inflation. Without COLA, the value of fixed benefits would erode over time, leaving beneficiaries with less real income. It’s an annual recalculation that aims to keep pace with the rising costs of goods and services that affect the everyday lives of retirees and other Social Security recipients.

The Social Security Administration (SSA) typically announces the COLA for the upcoming year in October, based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index measures changes in the prices of a basket of consumer goods and services, providing a benchmark for inflation. A higher CPI-W generally translates to a higher COLA, reflecting a period of increased living expenses.

Anúncios

How COLA is Calculated

The calculation of COLA involves comparing the average CPI-W for the third quarter of the current year (July, August, September) with the average CPI-W for the third quarter of the last year in which a COLA was effective. The percentage increase, if any, between these two periods determines the COLA. If there’s no increase in the CPI-W, or if it decreases, then no COLA is applied for that year. This methodology ensures that adjustments are directly tied to real-world changes in consumer prices, providing a degree of protection against inflation for beneficiaries.

- CPI-W as Benchmark: The Consumer Price Index for Urban Wage Earners and Clerical Workers is the primary economic indicator used.

- Third Quarter Data: July, August, and September CPI-W figures are averaged to determine the change.

- Year-over-Year Comparison: The current year’s third-quarter average is compared to the last COLA-effective year’s third-quarter average.

- Percentage Increase: The resulting percentage difference, if positive, becomes the COLA.

Understanding this process helps clarify why COLA figures fluctuate annually and are subject to economic conditions. The 2026 Social Security Adjustments, particularly the 3.5% COLA, are a direct reflection of current economic forecasts and inflationary trends, indicating a period where the cost of living is expected to rise for many Americans.

In essence, COLA acts as a vital safeguard, protecting the financial well-being of millions of Americans who depend on Social Security. Its annual adjustment is a dynamic response to economic realities, aiming to maintain the purchasing power of benefits as the economy evolves.

The Projected 3.5% COLA for 2026: What It Means

The projection of a 3.5% COLA for 2026 Social Security Adjustments represents a significant increase that will impact the monthly benefits received by millions of Americans. While not as high as some recent years, a 3.5% COLA is still substantial enough to make a noticeable difference in the budgets of retirees, disabled individuals, and survivors. This percentage means that for every $1,000 in monthly benefits, an individual would see an increase of $35.

This adjustment is a direct response to inflationary pressures observed in the economy, ensuring that the purchasing power of Social Security benefits doesn’t diminish. For many, this increase will help offset rising costs in areas such as groceries, utilities, and healthcare, which are often the largest expenditures for those on fixed incomes.

Impact on Average Benefits

To illustrate, let’s consider the average Social Security benefit. While the exact average benefit for 2026 will depend on various factors, assuming a hypothetical average benefit of $1,800 per month, a 3.5% COLA would translate to an additional $63 per month. Over the course of a year, this adds up to an extra $756. This seemingly modest monthly increase can be crucial for individuals managing tight budgets, providing a bit more breathing room for essential expenses.

- Increased Monthly Income: Direct boost to monthly Social Security checks.

- Offsetting Inflation: Helps maintain the real value of benefits against rising prices.

- Budgetary Relief: Provides additional funds for essential living expenses.

The 2026 Social Security Adjustments are particularly important because they occur in an economic climate where inflation remains a persistent concern. The 3.5% COLA is a recognition of these ongoing pressures, aiming to prevent beneficiaries from falling behind financially. It’s a measure that underscores the government’s commitment to supporting the economic stability of its most vulnerable populations.

Therefore, understanding the implications of this 3.5% COLA is vital for current beneficiaries and those planning for retirement. It provides a clearer picture of future income and helps in making informed financial decisions.

Who Benefits from the 2026 Social Security Adjustments?

The 2026 Social Security Adjustments, particularly the 3.5% COLA, are designed to benefit a wide range of individuals who receive Social Security payments. This includes retirees, disabled workers, and survivors. Essentially, anyone currently receiving a Social Security benefit will see their payments increase proportionally to the COLA, ensuring that their financial support continues to meet the rising cost of living.

Retirees constitute the largest group of beneficiaries. For them, the COLA ensures that their retirement income keeps pace with inflation, protecting their purchasing power over many years. Disabled workers, who rely on Social Security Disability Insurance (SSDI) for their income, will also experience this increase, offering crucial financial stability. Similarly, surviving spouses and children receiving survivor benefits will see their payments adjusted, providing additional support during challenging times.

Categories of Beneficiaries

The Social Security system is designed to provide a safety net for various life circumstances. Each category of beneficiary has unique needs, and the COLA plays a vital role in addressing those needs by preventing the erosion of benefit value due to inflation.

- Retired Workers: The largest group, receiving benefits based on their earnings history.

- Disabled Workers: Individuals who are unable to work due to a severe medical condition.

- Spouses and Dependents: Family members of retired or disabled workers, or deceased workers.

- Survivors: Spouses, children, or parents of deceased workers who meet certain criteria.

The universal application of the COLA across these beneficiary groups highlights its importance as a broad-based measure to support financial well-being. It’s not just about a single demographic but about ensuring a baseline of economic security for all who depend on Social Security.

Ultimately, the 2026 Social Security Adjustments with a 3.5% COLA serve to strengthen the safety net provided by Social Security, ensuring that all beneficiaries receive an income that reflects current economic realities. This broad impact underscores the program’s vital role in the financial landscape of the United States.

Financial Planning with the 2026 COLA in Mind

Incorporating the 2026 Social Security Adjustments and the projected 3.5% COLA into your financial planning is a smart move, whether you are already receiving benefits or are nearing retirement. While the COLA provides a welcome boost, it’s essential to understand how it fits into your broader financial picture. This adjustment can influence budgeting, investment strategies, and even healthcare expense planning.

For current beneficiaries, the increased monthly payment can offer a bit more flexibility. It might allow for slightly higher spending on discretionary items, or more importantly, it could help cover the rising costs of necessities. For those approaching retirement, understanding the potential COLA can help in projecting future income streams more accurately, allowing for better-informed decisions about when to claim benefits and how to supplement Social Security with other savings.

Budgeting and Spending Power

The 3.5% COLA directly enhances your spending power. It’s crucial to revisit your budget and allocate these additional funds wisely. Consider where inflation has hit hardest in your personal finances—perhaps groceries, transportation, or healthcare—and direct the COLA increase to these areas first. This proactive approach ensures that the adjustment effectively mitigates inflationary pressures on your household.

For future retirees, factoring in a realistic COLA projection, such as the 2026 Social Security Adjustments, can help in retirement income modeling. While future COLA amounts are never guaranteed, understanding the mechanism and historical trends allows for more robust planning. It encourages a deeper look into how Social Security benefits will integrate with pensions, 401(k)s, and other savings.

Healthcare Costs and Medicare Premiums

One critical aspect to consider is the interaction between COLA and Medicare premiums. Often, increases in Medicare Part B premiums are deducted directly from Social Security benefits. While the COLA increases your gross benefit, a portion of that increase might be offset by higher Medicare costs. It’s important to monitor these potential changes to understand your net benefit increase.

- Re-evaluate Budget: Adjust your monthly budget to account for the increased income.

- Consider Healthcare Costs: Factor in potential increases in Medicare Part B premiums.

- Long-Term Projections: Use COLA information to refine long-term retirement income forecasts.

- Consult Financial Advisor: Seek professional advice to optimize your financial strategy.

By taking these factors into account, individuals can make the most of the 2026 Social Security Adjustments, ensuring their financial plans remain resilient and responsive to economic changes. Proactive financial planning is key to maximizing the benefit of any COLA increase.

The Broader Economic Context of the 2026 COLA

The 2026 Social Security Adjustments, particularly the projected 3.5% COLA, do not occur in a vacuum. They are a direct reflection of broader economic trends and inflationary pressures impacting the United States. Understanding this larger context helps explain why the COLA is what it is and what it signifies for the national economy. Economic indicators such as inflation rates, wage growth, and consumer spending all play a role in shaping the COLA calculation.

In recent years, the economy has experienced periods of significant inflation, driven by various factors including supply chain disruptions, increased consumer demand, and geopolitical events. While inflation may have cooled from its peak, it remains a persistent concern. The 3.5% COLA for 2026 suggests that economists anticipate continued, albeit perhaps moderated, price increases across many sectors.

Inflationary Environment

The primary driver of any COLA is inflation. When the cost of goods and services rises, the purchasing power of a fixed income declines. The Social Security Administration’s use of the CPI-W is specifically designed to measure these changes for urban wage earners and clerical workers, a demographic that often faces similar economic challenges to many Social Security beneficiaries. A 3.5% COLA indicates that the CPI-W has shown a comparable increase, signaling ongoing inflationary pressures that affect everyday living expenses.

This inflationary environment impacts everything from the price of gasoline and groceries to housing and medical care. For Social Security beneficiaries, whose incomes may be largely fixed, a COLA is essential to prevent their financial situation from deteriorating.

Impact on the Social Security Trust Funds

While beneficial for recipients, COLA increases also have implications for the solvency of the Social Security trust funds. Larger COLA adjustments mean greater outflows from the trust funds, which can accelerate their projected depletion dates if not accompanied by corresponding increases in revenue. Policymakers continuously monitor these trends, and the 2026 Social Security Adjustments will be part of ongoing discussions about the long-term financial health of the program.

- Economic Indicator: COLA reflects current and projected inflation rates.

- Consumer Prices: Higher COLA suggests rising costs for goods and services.

- Trust Fund Solvency: Increased COLA impacts the long-term financial outlook of Social Security.

The 3.5% COLA, therefore, is not just a number; it’s a barometer of the nation’s economic health and its impact on the most vulnerable populations. It underscores the continuous balancing act between providing adequate benefits and ensuring the long-term sustainability of the Social Security system.

Navigating Potential Challenges and Optimizing Benefits

While the 2026 Social Security Adjustments, including the 3.5% COLA, are generally good news for beneficiaries, it’s also important to navigate potential challenges and actively seek ways to optimize your overall benefits. An increase in Social Security payments can sometimes have unintended consequences, such as affecting eligibility for other assistance programs or increasing tax liabilities. Being aware of these possibilities allows for proactive planning.

For example, some low-income assistance programs have income thresholds. A COLA increase, while beneficial for Social Security, might push some beneficiaries slightly above these thresholds, potentially reducing or eliminating other forms of aid. It’s crucial to understand the rules of any additional programs you rely on and assess how the COLA might impact your eligibility.

Taxation of Social Security Benefits

Another area to consider is the taxation of Social Security benefits. Depending on your total income, a portion of your Social Security benefits may be subject to federal income tax. An increased benefit due to COLA could potentially push you into a higher tax bracket or increase the taxable portion of your benefits. While this typically affects higher-income individuals, it’s a factor worth considering for anyone whose total income is near the taxation thresholds.

Understanding these thresholds and planning accordingly can help mitigate any unexpected tax burdens. Consulting with a tax professional can provide personalized advice on how the 2026 Social Security Adjustments might affect your specific tax situation.

Strategies for Maximizing Benefits

Beyond simply receiving the COLA, there are strategies beneficiaries can employ to maximize their overall financial well-being. These include reviewing other income sources, managing debt, and exploring opportunities for additional savings. For those not yet claiming benefits, the decision of when to start receiving Social Security remains one of the most significant factors in maximizing lifetime benefits.

- Review Program Eligibility: Assess how COLA affects other assistance programs.

- Understand Tax Implications: Be aware of potential changes to Social Security benefit taxation.

- Financial Consultations: Seek advice from tax and financial professionals.

- Holistic Financial Planning: Integrate COLA into broader income and expense management.

By proactively addressing these challenges and implementing sound financial strategies, beneficiaries can ensure that the 2026 Social Security Adjustments contribute positively to their long-term financial security, rather than introducing unforeseen complications. It’s about taking control of your financial future in light of these changes.

Looking Ahead: The Future of Social Security and COLA

The 2026 Social Security Adjustments, including the 3.5% COLA, offer a snapshot of the program’s current state and its responsiveness to economic conditions. However, the future of Social Security and its annual COLA adjustments is a subject of ongoing discussion and evolving economic forecasts. Understanding these long-term perspectives is crucial for both current and future beneficiaries, as it informs expectations and encourages proactive planning.

Forecasting future COLA amounts is inherently challenging, as they depend heavily on unpredictable economic factors, particularly inflation rates. While a 3.5% COLA for 2026 is a projection based on current data, future adjustments could be higher or lower depending on global and domestic economic shifts. This uncertainty underscores the importance of a diversified retirement income strategy, rather than solely relying on Social Security for financial stability.

Potential Reforms and Solvency Concerns

The long-term solvency of the Social Security trust funds remains a significant topic of debate among policymakers. Projections indicate that without legislative changes, the trust funds may be unable to pay 100% of promised benefits at some point in the future. While the 2026 COLA addresses immediate purchasing power, it also adds to the total benefit payout, intensifying the discussion around potential reforms.

These reforms could include various measures such as adjusting the full retirement age, modifying the COLA calculation method, or increasing the Social Security tax rate or the amount of earnings subject to taxation. While no immediate changes are imminent for 2026, these discussions are vital for the program’s long-term health and could impact future generations of beneficiaries.

Adaptability of the COLA Mechanism

Despite the challenges, the COLA mechanism itself has proven adaptable over the years, serving its purpose of protecting beneficiaries from inflation. Its reliance on the CPI-W ensures that adjustments are tied to real economic metrics, providing a transparent and consistent method for benefit increases. However, some critics argue that the CPI-W may not fully reflect the expenditure patterns of seniors, particularly regarding healthcare costs.

- Economic Volatility: Future COLA amounts are subject to unpredictable economic changes.

- Policy Debates: Ongoing discussions about Social Security’s long-term solvency and potential reforms.

- Alternative Indices: Consideration of other inflation measures that may better reflect senior spending.

Therefore, while the 2026 Social Security Adjustments offer immediate relief, maintaining an informed perspective on the broader economic and political landscape surrounding Social Security is essential for long-term financial planning. Staying updated on legislative proposals and economic forecasts will empower beneficiaries to make the best decisions for their financial future.

| Key Point | Brief Description |

|---|---|

| 3.5% COLA Projection | Anticipated Cost-of-Living Adjustment for 2026, increasing Social Security benefits. |

| Inflation Offset | COLA ensures benefits keep pace with rising costs of goods and services. |

| Beneficiary Impact | Affects retirees, disabled workers, and survivors, boosting their monthly income. |

| Financial Planning | Crucial for budgeting, tax considerations, and long-term retirement income projections. |

Frequently Asked Questions About 2026 Social Security Adjustments

The primary purpose of the Social Security Cost-of-Living Adjustment (COLA) is to protect the purchasing power of Social Security benefits. It ensures that the value of benefits does not erode over time due to inflation, allowing recipients to maintain their standard of living as the cost of goods and services rises.

The 2026 COLA percentage, like all COLA adjustments, is determined by comparing the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the current year (July, August, September) to the third quarter of the last year a COLA was enacted. The percentage increase becomes the COLA.

Yes, increases in Medicare Part B premiums are often deducted directly from Social Security benefits. While the 3.5% COLA will increase your gross benefit, a portion of that increase might be offset by higher Medicare costs, impacting your net benefit. It’s important to monitor these changes.

Yes, generally all individuals currently receiving Social Security benefits are eligible for the Cost-of-Living Adjustment. This includes retired workers, disabled workers, and survivors. The increase is applied universally to help all beneficiaries keep pace with inflation and maintain their financial stability.

To best prepare, review your current budget and financial plan, considering how the increased benefit might impact your overall income and any other assistance programs. Also, be aware of potential tax implications and consult with a financial advisor to optimize your strategy based on the 2026 adjustments.

Conclusion

The 2026 Social Security Adjustments, particularly the projected 3.5% COLA, represent a vital mechanism in safeguarding the financial well-being of millions of Americans. This increase is a direct response to ongoing inflationary pressures, aiming to ensure that the purchasing power of Social Security benefits remains intact. For retirees, disabled individuals, and survivors, this adjustment means a tangible boost to their monthly income, offering crucial support in managing daily expenses. Understanding the intricacies of COLA, its calculation, and its broader economic context is essential for effective financial planning. While the COLA provides immediate relief, beneficiaries are encouraged to integrate this change into a comprehensive financial strategy, considering potential impacts on taxes and other aid programs. Looking ahead, the adaptability of the COLA mechanism, alongside ongoing discussions about Social Security’s long-term solvency, underscores the dynamic nature of this critical program. Staying informed and proactive will empower individuals to navigate these adjustments successfully and secure their financial future.