Credit Score Optimization 2025: Boost Your Score by 50 Points

Anúncios

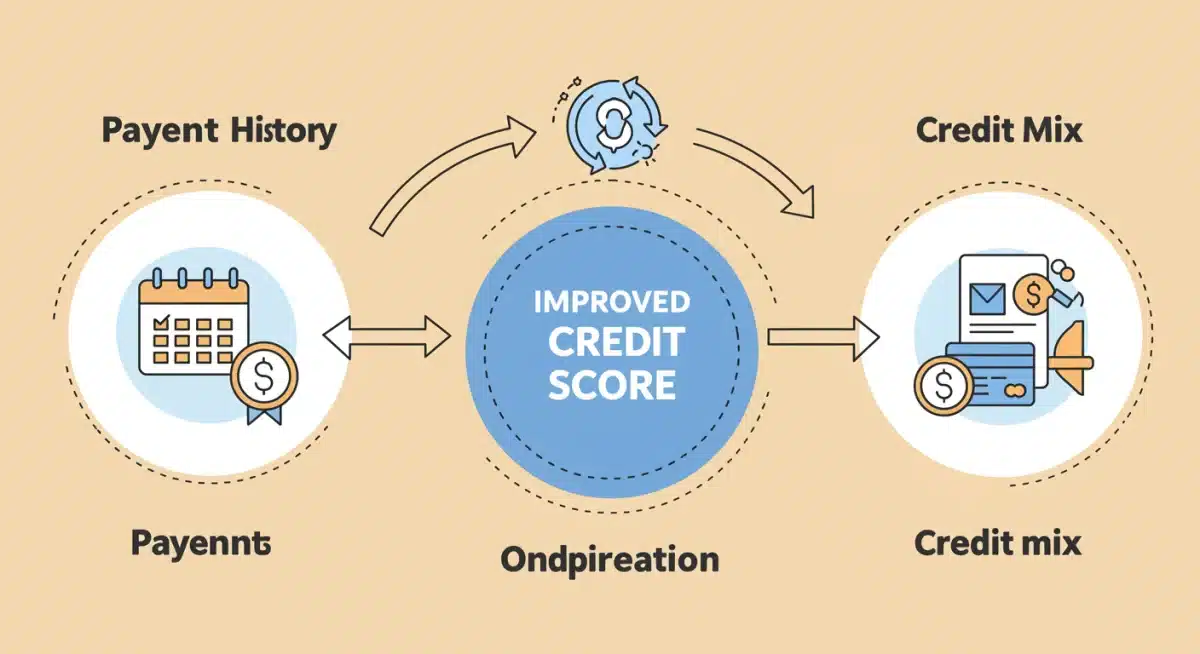

Achieving significant credit score improvement in 2025 is attainable by focusing on key strategies: maintaining an impeccable payment history, optimizing credit utilization below 30%, and diversifying your credit mix.

In the dynamic financial landscape of 2025, understanding and executing effective credit score optimization strategies is more critical than ever. Whether you’re aiming for a new home, a car, or simply better interest rates, a higher credit score opens doors. This guide will walk you through three proven strategies designed to help you boost your credit score by 50 points or more, setting you on a path to greater financial freedom.

Anúncios

Understanding the Foundation of Your Credit Score

Before diving into specific strategies, it’s essential to grasp what makes up your credit score. Your credit score is a numerical representation of your creditworthiness, primarily influenced by factors like payment history, amounts owed, length of credit history, new credit, and credit mix. Each of these components plays a significant role in determining your overall score, and understanding their weight is the first step toward effective optimization.

FICO and VantageScore are the two primary scoring models used by lenders. While they share many similarities, understanding their nuances can provide a strategic advantage. Both models prioritize responsible financial behavior, emphasizing the importance of consistent on-time payments and prudent credit management. Ignoring these foundational elements can undermine any optimization efforts, making it crucial to start with a solid understanding.

Anúncios

The FICO and VantageScore Models

While both models aim to assess credit risk, their weighting of factors can differ slightly. FICO is the most widely used model, with VantageScore gaining traction. Knowing which model a lender uses can sometimes help you tailor your approach, though generally, good credit habits benefit both.

- FICO Score: This model places significant emphasis on payment history (35%) and amounts owed (30%).

- VantageScore: While similar, it categorizes factors slightly differently, often highlighting payment history as ‘extremely influential’ and credit utilization as ‘highly influential.’

- Impact: Regardless of the model, consistent positive actions across all credit factors will lead to improvements.

Understanding these models helps demystify how your financial actions translate into a numerical score. It clarifies why certain behaviors, such as late payments, can have a disproportionately negative impact. By focusing on the areas that both models prioritize, you can ensure a comprehensive approach to credit score improvement.

Strategy 1: Master Your Payment History for Maximum Impact

Your payment history is the single most influential factor in your credit score, accounting for approximately 35% of your FICO score. Consistently making on-time payments demonstrates reliability and financial responsibility to lenders. Even a single missed payment can significantly drop your score and remain on your report for up to seven years. Therefore, mastering your payment history is paramount for any credit score optimization effort.

To ensure perfect payment behavior, consider setting up automatic payments for all your credit accounts. This eliminates the risk of forgetting a payment due date, which is a common pitfall. Additionally, if you’re struggling to make a payment, contact your creditor immediately to discuss potential solutions, such as a temporary payment plan. Proactive communication can sometimes prevent a late payment from being reported to credit bureaus.

Automate for Success

Automation is your best friend when it comes to payment history. Setting up recurring payments ensures that you never miss a due date, even if you’re busy or traveling. This simple step can prevent significant damage to your credit score and save you from late fees.

- Set up autopay: Enroll in automatic payments through your bank or creditor’s online portal.

- Choose the right amount: Opt to pay the full statement balance to avoid interest, or at least the minimum payment to prevent late marks.

- Monitor your accounts: Even with automation, regularly check your accounts to ensure payments are processed correctly.

Beyond automation, actively reviewing your credit report for any inaccuracies related to payment history is crucial. Errors can occur, and an incorrectly reported late payment can unfairly drag down your score. Disputing such errors promptly can lead to their removal and a subsequent score increase.

Strategy 2: Optimize Your Credit Utilization Ratio

Credit utilization, or the amount of credit you’re using compared to your total available credit, is the second most important factor, making up about 30% of your FICO score. A high utilization ratio signals to lenders that you might be over-reliant on credit, which can be seen as a risk. The general rule of thumb is to keep your credit utilization below 30% across all your accounts. For optimal results, many experts recommend aiming for under 10%.

Reducing your credit utilization involves a two-pronged approach: paying down your balances and, if appropriate, increasing your credit limits. Paying down high-interest debt first can free up more funds to tackle other balances. When requesting a credit limit increase, ensure it’s a soft inquiry that won’t negatively impact your score, and only do so if you can resist the temptation to spend more.

Key Actions to Lower Utilization

Proactively managing your credit card balances is key to maintaining a healthy utilization ratio. This requires discipline and a clear understanding of your spending habits.

- Pay down balances: Focus on reducing the amount you owe on your credit cards.

- Make multiple payments: Instead of one large payment at the end of the month, consider making smaller payments throughout the billing cycle to keep your reported utilization low.

- Increase credit limits: If you have a good payment history, request a credit limit increase. This boosts your available credit without increasing your debt, lowering your utilization ratio.

Be mindful of when your credit card companies report your balances to credit bureaus. Often, they report the balance on your statement closing date. Paying down your balance before this date can ensure a lower utilization ratio is reported, positively impacting your score.

Strategy 3: Diversify Your Credit Mix and Extend Credit History

While not as heavily weighted as payment history or utilization, your credit mix (around 10% of FICO) and length of credit history (around 15%) contribute significantly to a robust credit score. Lenders prefer to see a healthy mix of different types of credit, such as revolving credit (credit cards) and installment loans (mortgages, auto loans, student loans). This demonstrates your ability to manage various forms of debt responsibly. Furthermore, a longer credit history generally indicates more experience and less risk.

To improve your credit mix, consider opening a new type of account if it aligns with your financial needs and you can manage it responsibly. For instance, if you only have credit cards, a small personal loan can diversify your profile. However, avoid opening too many new accounts in a short period, as this can temporarily lower your score due to hard inquiries and a shorter average age of accounts.

Building a Strong Credit Profile

Strategic account management and patience are crucial for enhancing your credit mix and history. Avoid closing old accounts, even if they are paid off, as this can shorten your average credit history.

- Maintain diverse accounts: A mix of credit cards, auto loans, and mortgages showcases responsible management of different credit types.

- Keep old accounts open: The longer your credit history, the better. Resist the urge to close old, paid-off credit card accounts, as this can reduce your average account age.

- Be patient with new credit: When you open a new account, it initially lowers your average account age. The positive impact of diversification grows over time.

Focus on gradually building a diverse and long-standing credit profile. This isn’t a quick fix but a long-term strategy that yields substantial benefits. Regularly reviewing your credit report will help you identify opportunities to strengthen your credit mix and ensure accuracy.

Monitoring Your Progress and Avoiding Pitfalls

Regularly monitoring your credit report and score is a crucial, often overlooked, aspect of credit score optimization. By keeping a close eye on your credit health, you can quickly identify any discrepancies, fraudulent activity, or areas that need improvement. The financial landscape is constantly evolving, and staying informed about your credit standing ensures you can adapt your strategies as needed.

Many credit card companies and financial institutions now offer free credit score monitoring services, providing easy access to your scores and reports. Additionally, you are entitled to a free credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months through AnnualCreditReport.com. Take advantage of these resources to stay on top of your credit.

Common Credit Score Pitfalls to Avoid

While focusing on positive actions, it’s equally important to be aware of behaviors that can negatively impact your score. Avoiding these common pitfalls can prevent setbacks in your credit optimization journey.

- Applying for too much new credit: Each hard inquiry can temporarily lower your score. Only apply for credit when genuinely needed.

- Closing old credit accounts: This can reduce your total available credit and shorten your average credit history, both negatively impacting your score.

- Ignoring small balances: Even a small, forgotten balance can lead to a missed payment and a significant score drop.

Maintaining vigilance and proactively managing your credit is an ongoing process. By understanding the factors that influence your score and actively avoiding common mistakes, you can sustain your credit health and continue to see improvements over time. This continuous monitoring is a cornerstone of effective financial management in 2025.

Advanced Tactics for Rapid Credit Score Improvement

While the foundational strategies of payment history, credit utilization, and credit mix form the bedrock of credit score optimization, several advanced tactics can accelerate your progress, especially if you’re looking for a significant boost. These methods often require a bit more understanding or specific financial situations but can yield impressive results when applied correctly. They move beyond the basics to fine-tune your credit profile for maximum impact.

One such tactic involves becoming an authorized user on an account with excellent payment history and low utilization. This can immediately add positive credit history to your report, especially beneficial for those with thin credit files. However, ensure the primary account holder is financially responsible, as their missteps could also affect your score. Another advanced approach is utilizing credit builder loans, specifically designed to help individuals establish or rebuild credit by demonstrating consistent payments on a small, secured loan.

Leveraging Credit Builder Tools

Credit builder tools are innovative financial products designed to help individuals with limited or poor credit history to establish or improve their scores. These can be particularly effective when traditional credit options are unavailable.

- Secured credit cards: These require a security deposit, which often becomes your credit limit. They report to credit bureaus, helping you build positive payment history.

- Credit builder loans: These loans hold the funds in a savings account while you make payments. Once paid off, you receive the funds, and your payment history is reported.

- Experian Boost and similar services: These services can incorporate utility and phone payments into your credit report, potentially increasing your score.

These advanced strategies, when combined with diligent application of the core principles, can significantly shorten the time it takes to achieve your credit score goals. They offer targeted solutions for specific scenarios, allowing for a more tailored and aggressive approach to credit score optimization. Always research and understand the terms before committing to any new financial product.

Long-Term Financial Health and Credit Score Resilience

Achieving a high credit score is not merely about reaching a numerical target; it’s about establishing long-term financial health and resilience. A strong credit score is a reflection of responsible financial habits that extend beyond just credit management. It indicates an ability to manage debt, save for the future, and make informed financial decisions. In 2025, with economic uncertainties, building this resilience is more important than ever to navigate financial challenges with confidence.

Developing a comprehensive financial plan that includes budgeting, saving, and investing alongside credit management is crucial. A budget helps you understand your income and expenses, preventing overspending that could lead to credit card debt. Savings provide a buffer for emergencies, reducing the likelihood of relying on credit during unforeseen circumstances. Investing, even modestly, builds wealth over time, further solidifying your financial foundation.

Integrating Credit into Your Overall Financial Plan

Your credit score should be an integral part of your larger financial strategy. It impacts everything from loan approvals to insurance premiums and even employment opportunities.

- Budgeting for credit payments: Ensure your budget allocates sufficient funds for all credit payments, preferably paying more than the minimum.

- Emergency fund: Build an emergency fund to avoid using credit cards for unexpected expenses, which can lead to high utilization.

- Financial education: Continuously educate yourself on personal finance to make informed decisions and adapt to changing economic conditions.

By viewing credit score optimization as a component of your broader financial well-being, you foster habits that lead to sustained success. This holistic approach ensures that your credit score not only improves but remains robust, providing you with financial flexibility and peace of mind for years to come. The effort invested now will pay dividends in your financial future.

| Key Strategy | Brief Description |

|---|---|

| Master Payment History | Always pay bills on time; set up autopay to avoid missed payments, as this is 35% of your score. |

| Optimize Credit Utilization | Keep credit card balances below 30% (ideally 10%) of your total available credit to positively impact 30% of your score. |

| Diversify Credit Mix | Maintain a healthy blend of revolving and installment accounts, contributing to 10-15% of your score. |

| Monitor Credit Regularly | Check credit reports for errors and track progress to ensure strategies are effective and identify issues promptly. |

Frequently Asked Questions About Credit Score Optimization

Significant improvements can often be seen within 3-6 months of implementing consistent positive credit habits. Minor changes might appear sooner, especially if you address high credit utilization quickly. Long-term strategies like building credit history take more time to fully mature.

No, checking your own credit score (a “soft inquiry”) does not harm it. Lenders performing a credit check for a loan application (a “hard inquiry”) can slightly lower your score temporarily, but the impact is usually minimal and short-lived.

Generally, no. Closing old credit cards can reduce your overall available credit, increasing your credit utilization ratio, and shorten your average length of credit history, both of which can negatively impact your credit score. Keep them open if they don’t have annual fees.

A good credit utilization ratio is typically below 30%. For excellent scores, aiming for under 10% is often recommended. This ratio compares your total credit card balances to your total available credit across all your revolving accounts.

Yes, absolutely. While bankruptcy remains on your report for 7-10 years, you can rebuild your credit. Focus on establishing new positive credit history through secured cards, credit-builder loans, and consistent, on-time payments. Time and responsible behavior are key.

Conclusion

Achieving significant credit score optimization in 2025 is an attainable goal for anyone committed to financial improvement. By diligently focusing on the three core strategies—mastering your payment history, optimizing your credit utilization, and diversifying your credit mix—you can realistically boost your score by 50 points or more. Remember that credit building is a marathon, not a sprint, requiring consistent effort and smart financial decisions. Regularly monitor your progress, avoid common pitfalls, and integrate credit management into your broader financial plan to secure a resilient and prosperous financial future.

Match: Boost Retirement Benefits by 15% in 2025")