Small Business Financing 2026: 4% Lower Interest Rates in US

Anúncios

In 2026, small businesses in the US can anticipate a unique opportunity to access capital with interest rates potentially 4% lower than previous years, driven by evolving economic policies and innovative lending solutions.

The year 2026 presents a pivotal moment for entrepreneurs, with the landscape of Small Business Financing in 2026: Accessing Capital with a 4% Lower Interest Rate in the US Market opening up unprecedented opportunities. This significant reduction in interest rates could be a game-changer for growth, expansion, and stability across various sectors.

Anúncios

Understanding the Economic Climate for Lower Rates

The economic forecast for 2026 suggests a stabilization and potential easing of monetary policies, creating a favorable environment for borrowing. After a period of fluctuating interest rates, indicators point towards a more predictable and advantageous lending climate for small and medium-sized enterprises (SMEs) across the United States. This shift is not arbitrary; it’s a result of a combination of factors, including inflation control measures taking hold and a concerted effort by financial institutions to stimulate economic activity.

Government policies and central bank strategies are playing a crucial role in shaping this new financial reality. Anticipated adjustments in federal interest rates, coupled with incentives for banks to lend to small businesses, are expected to drive down the cost of capital. This proactive approach aims to empower businesses to invest in innovation, expand operations, and create jobs, thereby fostering robust economic growth.

Anúncios

Key Economic Indicators

Several economic indicators are signaling this positive trend. A steady decline in the inflation rate, coupled with stable employment figures, provides the Federal Reserve with the flexibility to consider more accommodative monetary policies. Furthermore, global economic stability, while always subject to change, is projected to be more favorable, reducing external pressures that might otherwise lead to tighter credit conditions.

- Inflation Control: Successful management of inflation allows for interest rate adjustments.

- Stable Employment: A strong job market supports consumer spending and business confidence.

- Government Incentives: Programs designed to encourage small business lending.

- Global Economic Stability: Reduced external volatility contributes to domestic financial predictability.

In essence, the economic climate in 2026 is poised to offer small businesses a significant advantage. The anticipated 4% lower interest rate is not merely a number; it represents a tangible reduction in the cost of doing business, freeing up capital that can be reinvested into the business rather than being allocated to higher interest payments.

Navigating Traditional Lending with New Advantages

Traditional banks, often seen as the backbone of small business financing, are adapting to the evolving economic landscape. While their processes may still be more rigorous than alternative lenders, the prospect of 4% lower interest rates makes them an even more attractive option for eligible businesses. Banks are expected to roll out new loan products and refine existing ones to align with the more favorable interest rate environment, seeking to capture a larger share of the small business market.

Securing a traditional bank loan in 2026 will still require a solid business plan, strong credit history, and comprehensive financial statements. However, the reduced cost of borrowing could lead to more lenient terms in other areas, such as collateral requirements or repayment schedules, as banks compete for borrowers. Building a strong relationship with a local bank can also provide access to personalized advice and potentially better terms.

Tips for Approaching Banks

Preparing thoroughly before approaching a bank is more critical than ever, especially when aiming to capitalize on lower interest rates. A well-presented case can significantly improve a business’s chances of approval and securing the most advantageous terms.

- Detailed Business Plan: Outline your strategy, market analysis, and financial projections.

- Strong Credit Score: Ensure both personal and business credit scores are optimized.

- Comprehensive Financials: Provide up-to-date balance sheets, income statements, and cash flow projections.

- Clear Use of Funds: Articulate exactly how the loan will be used and its expected return on investment.

The traditional lending sector, while maintaining its foundational principles, is becoming increasingly competitive. Small businesses that present a clear, compelling case for financing will be best positioned to take advantage of the anticipated lower interest rates.

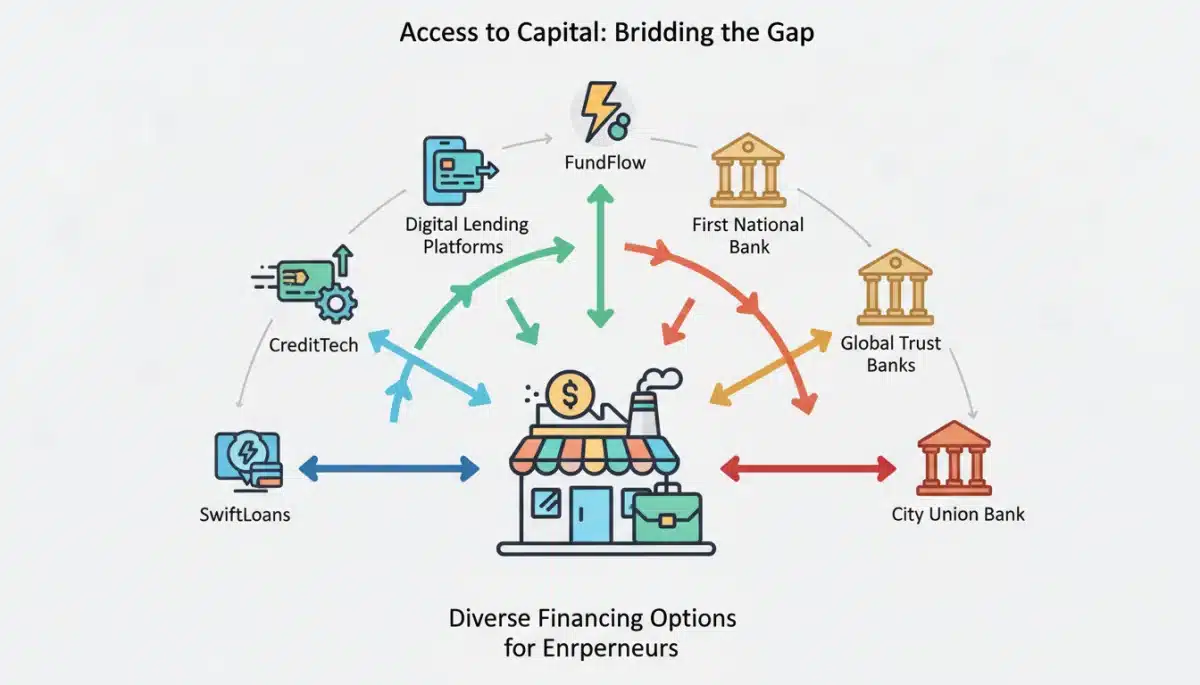

The Rise of Alternative Lending and Fintech Solutions

Beyond traditional banks, the alternative lending landscape continues to evolve rapidly, offering diverse and often more flexible financing options. In 2026, fintech companies and online lenders are expected to play an even more significant role, particularly in providing access to capital for businesses that might not meet stringent traditional bank criteria. The competitive pressure from these innovative platforms is also a contributing factor to the overall downward trend in interest rates.

These platforms leverage advanced algorithms and data analytics to assess creditworthiness, often providing quicker approvals and disbursements. While their interest rates historically have been higher than traditional banks, the general market shift towards lower rates will likely extend to this sector, making them even more viable for a broader range of small businesses. Options include online term loans, lines of credit, invoice financing, and merchant cash advances.

Advantages of Fintech Lending

Fintech solutions are renowned for their speed, convenience, and ability to cater to niche markets. For businesses looking for rapid access to funds or those with less conventional financial histories, these platforms can be invaluable. The streamlined application processes and reduced paperwork are often cited as major benefits.

- Speed and Efficiency: Faster application and approval processes.

- Flexible Criteria: More accommodating for businesses with less-than-perfect credit.

- Diverse Products: A wider array of specialized financing options.

- Convenience: Online-first approach reduces administrative burden.

As the market matures, the distinction between traditional and alternative lenders may blur, with both sectors offering increasingly competitive rates and tailored solutions. Small businesses should explore all avenues to find the financing that best suits their unique needs and leverage the predicted lower interest rates.

Government-Backed Programs: SBA Loans and Beyond

Government initiatives, particularly those from the Small Business Administration (SBA), remain a cornerstone of small business financing in the US. In 2026, these programs are anticipated to be even more impactful, especially with the reduced interest rate environment. SBA loans, known for their favorable terms and lower down payments, will likely become even more attractive, providing a crucial lifeline for many entrepreneurs.

The SBA offers various loan programs, including the popular 7(a) loan, 504 loan, and microloan programs, each designed to meet different business needs. These loans are typically disbursed through traditional lenders but are partially guaranteed by the government, reducing the risk for banks and encouraging them to lend to small businesses. This guarantee mechanism is particularly effective in a lower interest rate climate, as banks can offer more competitive rates with less exposure.

Key SBA Programs to Consider

Understanding the different SBA programs is vital for businesses seeking government-backed financial assistance. Each program has specific eligibility requirements and uses for funds, making it important to match the right program to the business’s goals.

- SBA 7(a) Loans: Most common, versatile for various business needs, up to $5 million.

- SBA 504 Loans: For purchasing major assets like real estate or machinery, promoting economic development.

- SBA Microloans: Smaller loans, up to $50,000, for startups and small businesses.

- Disaster Loans: For businesses impacted by declared disasters, offering low-interest rates.

Beyond the SBA, other federal and state programs may emerge or expand in 2026, offering grants, tax incentives, or specialized loans for specific industries or demographics. Staying informed about these government-backed opportunities is crucial for maximizing access to capital at a lower cost.

Strategic Planning for Optimal Capital Access

Accessing capital with a 4% lower interest rate in 2026 requires more than just knowing where to look; it demands strategic planning and meticulous preparation. Businesses that proactively assess their financial health, refine their business models, and understand their funding needs will be best positioned to secure the most favorable terms. This proactive approach helps in presenting a compelling case to lenders and taking full advantage of the market conditions.

A critical component of strategic planning involves forecasting future cash flows and understanding the true cost of borrowing. Even with lower interest rates, businesses must ensure they can comfortably meet repayment obligations without straining operations. This includes creating realistic projections and contingency plans for unexpected challenges. Furthermore, exploring different loan structures, such as fixed versus variable rates, can help tailor financing to specific business risk appetites.

Developing a Robust Financial Strategy

A well-thought-out financial strategy is the bedrock of successful capital acquisition. It involves a holistic view of the business’s financial situation and its future aspirations. This strategy should be dynamic, adapting to market changes and internal growth.

- Financial Health Assessment: Regularly review balance sheets, income statements, and cash flow.

- Clear Funding Needs: Precisely define how much capital is needed and for what purpose.

- Credit Score Management: Actively work to improve and maintain excellent credit scores.

- Lender Relationship Building: Establish connections with various financial institutions before needing funds.

Ultimately, strategic planning in 2026 means approaching financing with a clear vision and a well-documented plan. Businesses that demonstrate financial prudence and a clear path to profitability will find lenders more willing to offer competitive rates and terms, fully capitalizing on the anticipated 4% interest rate reduction.

Future Trends and What to Expect in 2026

Looking ahead to 2026, several key trends are expected to shape the landscape of small business financing. Beyond the anticipated 4% lower interest rates, advancements in technology, evolving regulatory frameworks, and a greater emphasis on sustainable and impact investing will influence how businesses access and utilize capital. Staying abreast of these trends can provide a competitive edge in securing funding.

The continued digitalization of financial services will streamline lending processes even further, making it easier and faster for businesses to apply for and receive funds. Artificial intelligence and machine learning will enhance credit risk assessment, potentially opening doors for businesses with non-traditional credit histories. Moreover, there’s a growing movement towards impact investing, where lenders consider a business’s social and environmental contributions alongside financial metrics, potentially offering favorable terms to align with these values.

Emerging Lending Innovations

The financial sector is continuously innovating, and 2026 will likely see the mainstream adoption of several emerging lending models. These innovations are designed to address the diverse needs of small businesses and offer more tailored financial solutions.

- Embedded Finance: Lending integrated directly into business software or platforms.

- Revenue-Based Financing: Repayment tied to a percentage of future revenue, offering flexibility.

- Blockchain-Based Lending: Decentralized lending platforms for increased transparency and efficiency.

- Green Loans: Specialized financing for businesses focused on environmental sustainability.

The future of small business financing in 2026 is dynamic and full of opportunities. Businesses that embrace technological advancements, adapt to new lending models, and align with evolving investor priorities will be well-positioned to thrive in this new financial era, especially with the added benefit of lower interest rates.

| Key Point | Brief Description |

|---|---|

| Lower Interest Rates | Anticipated 4% reduction in interest rates for small business loans in 2026. |

| Economic Climate | Stabilizing inflation and government policies create favorable lending conditions. |

| Diverse Lending Options | Traditional banks, fintech, and government-backed programs offer varied capital access. |

| Strategic Preparation | Proactive financial planning and strong credit are key to securing favorable terms. |

Frequently Asked Questions About 2026 Small Business Financing

The projected lower interest rates in 2026 are primarily driven by anticipated stabilization of inflation, more accommodative monetary policies from the Federal Reserve, and government incentives aimed at stimulating small business lending. Global economic stability also plays a role in fostering a more predictable financial environment for borrowers.

To best prepare, small businesses should focus on maintaining a strong credit score, developing a detailed business plan with clear financial projections, and understanding their precise funding needs. Building relationships with various lenders, both traditional and alternative, can also provide a strategic advantage when seeking capital.

Both traditional banks and alternative lenders are expected to offer more competitive rates due to the overall market shift. While traditional banks may still offer the lowest rates for highly qualified borrowers, fintech lenders will likely become more competitive, making them a strong option for businesses seeking speed and flexibility.

Government-backed programs, particularly SBA loans, will remain crucial. With lower interest rates, SBA loans will become even more attractive, as their government guarantee reduces risk for lenders, allowing them to offer favorable terms to a wider range of small businesses for various purposes, from expansion to equipment purchase.

Beyond interest rates, businesses should monitor the growth of embedded finance, revenue-based financing, and blockchain-based lending for innovative capital access. Additionally, the increasing focus on sustainable and impact investing could unlock new funding opportunities for businesses aligning with environmental and social governance criteria, influencing lending terms and availability.

Conclusion

The outlook for Small Business Financing in 2026: Accessing Capital with a 4% Lower Interest Rate in the US Market is exceptionally promising. This anticipated reduction in borrowing costs presents a significant opportunity for small businesses to fuel their growth, invest in innovation, and solidify their market position. By understanding the economic drivers, exploring diverse lending avenues, and engaging in meticulous strategic planning, entrepreneurs can effectively navigate this favorable financial landscape. The convergence of stabilizing economic conditions, evolving lending technologies, and supportive government policies creates a unique window for businesses to secure capital on terms that were previously unattainable, paving the way for a more robust and dynamic small business sector in the United States.