ACA 2026: Premium Tax Credits & Subsidies Explained

Anúncios

The Affordable Care Act (ACA) in 2026 continues to provide essential financial assistance, primarily through premium tax credits and subsidies, to help eligible Americans afford health insurance coverage.

As we look towards 2026, understanding the nuances of the Affordable Care Act (ACA) 2026: Understanding Premium Tax Credits and Subsidies for Health Insurance Benefits remains crucial for millions of Americans seeking affordable healthcare. This comprehensive guide will demystify the mechanisms of financial assistance available, helping you make informed decisions about your health insurance.

Anúncios

The Foundation of ACA: Ensuring Access to Healthcare

The Affordable Care Act, often referred to as Obamacare, was signed into law in 2010 with the primary goal of expanding access to affordable health insurance. It introduced a range of reforms designed to make health insurance markets fairer and more transparent, while also providing financial assistance to individuals and families who qualify. The ACA established Health Insurance Marketplaces, or exchanges, where people can compare and purchase health insurance plans.

Beyond market regulation, a cornerstone of the ACA is its provision for financial help. This aid comes in two main forms: premium tax credits and cost-sharing reductions. These mechanisms are designed to lower the monthly premiums and out-of-pocket expenses, respectively, making health coverage a realistic option for those who might otherwise find it unaffordable. The ongoing evolution of the ACA means that understanding these provisions in 2026 is as vital as ever, especially with potential adjustments and expansions.

Anúncios

The ACA’s impact has been significant, reducing the uninsured rate in the United States to historic lows. It mandates that most health plans cover a set of essential health benefits, ranging from preventive care and maternity services to mental health and prescription drugs. This ensures that even with financial assistance, individuals are receiving comprehensive coverage, not just basic catastrophic plans. Staying informed about these benefits and how they apply to your situation is key to maximizing your healthcare opportunities.

Unpacking Premium Tax Credits in 2026

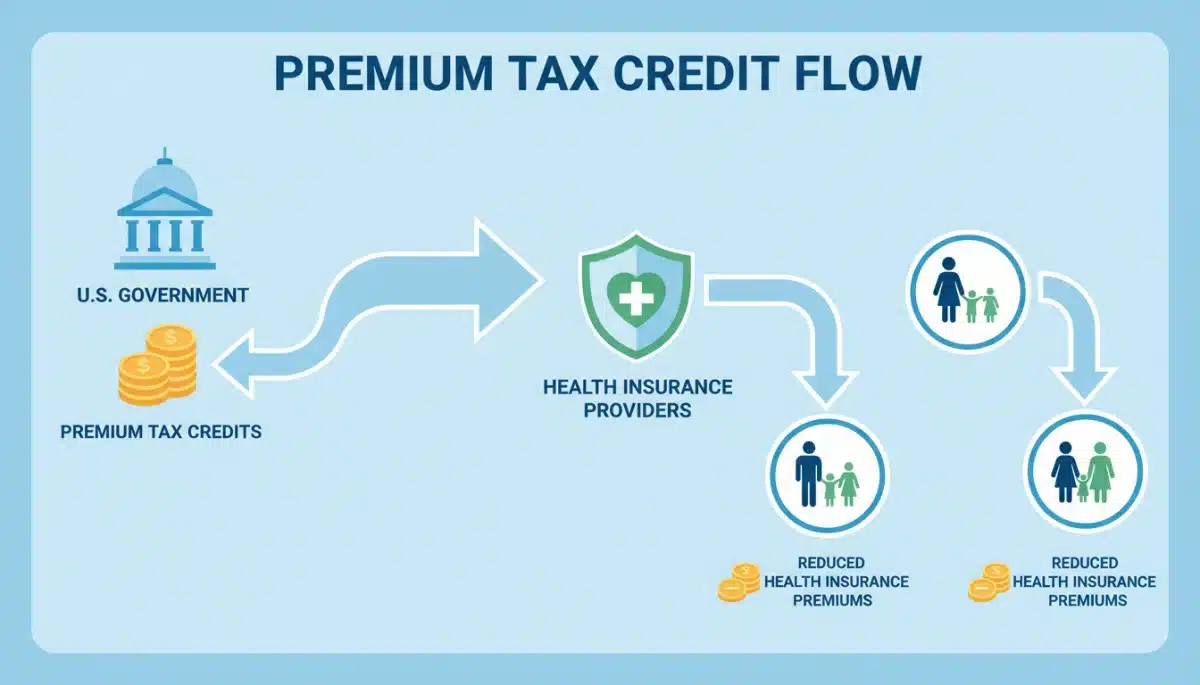

Premium tax credits, also known as premium subsidies, are a critical component of the Affordable Care Act, designed to help individuals and families pay for their health insurance premiums. These credits reduce the amount you have to pay each month for health insurance purchased through the Health Insurance Marketplace. The amount of the credit is based on your income and household size, ensuring that coverage remains affordable relative to your financial situation. For 2026, the eligibility criteria and calculation methods for these credits are expected to largely follow the established framework, with potential legislative adjustments.

Eligibility for Premium Tax Credits

To qualify for premium tax credits, your household income must fall within a certain range relative to the federal poverty level (FPL). Typically, individuals and families with incomes between 100% and 400% of the FPL are eligible. However, legislative changes, such as those introduced in recent years, have temporarily expanded eligibility, allowing more people to qualify and receive larger subsidies. It’s crucial to check the specific FPL guidelines for 2026, as these are updated annually.

- Income Thresholds: Generally, incomes between 100% and 400% of the FPL are eligible, though temporary expansions might broaden this.

- Marketplace Enrollment: You must purchase your health insurance plan through a state or federal Health Insurance Marketplace.

- No Employer-Sponsored Coverage: You cannot be eligible for affordable employer-sponsored health coverage that meets minimum value standards.

- Not Eligible for Public Programs: You must not be eligible for Medicare, Medicaid, CHIP, or other public health coverage programs.

The amount of your premium tax credit is calculated on a sliding scale. This means that individuals and families with lower incomes receive larger credits, effectively capping their premium contributions at a certain percentage of their income. This mechanism ensures that even those with modest incomes can access quality health insurance without undue financial burden. Understanding how your income and household size factor into this calculation is essential for estimating your potential savings.

How Subsidies Work: Reducing Your Healthcare Costs

Beyond premium tax credits, the ACA also offers cost-sharing reductions (CSRs), which are another form of subsidy aimed at making healthcare more affordable. While premium tax credits lower your monthly payments, CSRs reduce the amount you have to pay out-of-pocket when you use healthcare services. This includes deductibles, co-payments, and co-insurance. CSRs are available to individuals and families with incomes below 250% of the federal poverty level who enroll in a silver-level plan through the Marketplace. These subsidies are automatically applied if you qualify, directly lowering your financial responsibility at the point of care.

The design of CSRs is particularly beneficial for those who frequently use healthcare services, as they can significantly reduce the financial burden associated with medical treatments and prescriptions. Unlike premium tax credits, which can be received in advance or claimed at tax time, CSRs are integrated into specific silver-level plans. This means that if you qualify for CSRs, you must choose a silver plan to receive these benefits, as they are not available with bronze, gold, or platinum plans. This linkage ensures that the plans offering CSRs also provide a good balance of premium and out-of-pocket costs.

It’s important to note that while premium tax credits directly reduce your monthly premium, CSRs affect the actuarial value of your plan. This means that a silver plan with CSRs will cover a higher percentage of your healthcare costs than a standard silver plan. For example, a standard silver plan covers about 70% of your costs, but with CSRs, it might cover 73%, 87%, or even 94%, depending on your income level. This enhanced coverage can translate into substantial savings over the course of a year, especially if unexpected medical needs arise.

In essence, these subsidies work in tandem to create a robust financial safety net within the ACA. Premium tax credits address the upfront cost of insurance, while CSRs tackle the expenses incurred during actual healthcare utilization. This dual approach aims to ensure that health insurance is not just affordable to buy, but also affordable to use. Careful consideration of both types of assistance is crucial when selecting a health plan in 2026, especially for those with lower incomes.

Navigating the Health Insurance Marketplace in 2026

The Health Insurance Marketplace, also known as the exchange, serves as the central hub for individuals and families to shop for and enroll in health insurance plans that comply with the Affordable Care Act. In 2026, this platform will continue to be the primary gateway for accessing premium tax credits and cost-sharing reductions. Understanding how to effectively navigate the Marketplace is fundamental to securing affordable and comprehensive health coverage tailored to your needs.

Key Steps for Enrollment

Enrolling through the Marketplace involves several straightforward steps, starting with creating an account and providing basic demographic and income information. This data is essential for determining your eligibility for financial assistance. The Marketplace then presents you with a range of plans, categorized by metal levels (Bronze, Silver, Gold, Platinum), each offering different levels of coverage and cost-sharing. It’s crucial to compare these plans not just on their monthly premiums, but also on their deductibles, co-pays, and out-of-pocket maximums.

- Account Creation: Set up your secure account on HealthCare.gov or your state’s exchange.

- Eligibility Determination: Provide household income and size to determine subsidy eligibility.

- Plan Comparison: Review various plans by metal level, considering premiums, deductibles, and out-of-pocket costs.

- Enrollment: Select the plan that best fits your healthcare needs and budget.

The Marketplace also offers tools and resources, including calculators and direct assistance from trained navigators or brokers, to help you understand your options. These resources can be invaluable, especially if you’re new to the Marketplace or if your financial or family situation has changed. Open enrollment periods are specific times of the year when you can sign up for a new plan or change your existing one. However, certain life events, such as marriage, birth of a child, or loss of other coverage, may qualify you for a Special Enrollment Period outside of the standard window.

Choosing the right plan involves balancing premiums with potential out-of-pocket costs. For those eligible for cost-sharing reductions, a silver plan is often the most advantageous choice, as it combines lower premiums (due to premium tax credits) with reduced deductibles and co-pays. The Marketplace aims to simplify this complex decision-making process, ensuring that consumers can find a plan that not only fits their budget but also provides adequate coverage for their medical needs in 2026.

Impact of Income Changes on ACA Benefits

A significant aspect of receiving financial assistance through the ACA is its direct correlation with your household income. Since premium tax credits and cost-sharing reductions are income-based, any substantial change in your income can directly impact the amount of financial help you receive. This dynamic nature requires individuals and families to proactively report income changes to the Health Insurance Marketplace to ensure they are receiving the correct level of subsidies and avoid potential issues at tax time.

Reporting Income Adjustments

If your income increases, you might become eligible for a smaller tax credit, or even lose eligibility altogether. Failing to report an income increase could result in you having to repay some or all of the excess premium tax credits you received when you file your federal income tax return. Conversely, if your income decreases, you might be eligible for a larger tax credit, which could reduce your monthly premiums. Reporting this change promptly can provide immediate financial relief. It’s not just income from employment that counts; changes in unemployment benefits, Social Security, or self-employment income also need to be considered.

The Marketplace is designed to adjust your subsidies throughout the year as your financial situation evolves. This flexibility is crucial for maintaining affordable coverage. For instance, if you get a new job with a higher salary, updating your income information allows the Marketplace to re-calculate your premium tax credit, potentially increasing your monthly premium but preventing a large repayment obligation later. Similarly, if you lose a job, reporting the income reduction can lead to lower premiums, helping you maintain coverage during a difficult period.

- Income Increases: May reduce your premium tax credit, potentially leading to repayment at tax time if not reported.

- Income Decreases: Could increase your premium tax credit, lowering your monthly payments if reported promptly.

- Household Changes: Marriage, divorce, birth, or adoption can also affect eligibility and subsidy amounts.

- Tax Implications: Annual reconciliation of premium tax credits with actual income is done during tax filing.

Monitoring and reporting income changes is not just a recommendation; it’s a responsibility. The IRS reconciles the advance premium tax credits you received with your actual income when you file your taxes. An accurate and timely update of your income information with the Marketplace minimizes the risk of owing money back to the IRS or missing out on additional financial assistance you might be entitled to. Staying vigilant about your financial status and its implications for your ACA benefits is a smart strategy for 2026.

Essential Health Benefits and Plan Tiers

The Affordable Care Act mandates that all health plans offered through the Marketplace, and most plans outside of it, cover a comprehensive set of ten categories of essential health benefits (EHBs). This provision ensures that consumers receive robust coverage, regardless of the plan tier they choose. Understanding these EHBs and how they are integrated into different plan tiers (Bronze, Silver, Gold, Platinum) is crucial for making an informed decision about your health insurance in 2026.

The Ten Essential Health Benefits

These benefits cover a broad range of services deemed fundamental for health and well-being. They include ambulatory patient services (outpatient care), emergency services, hospitalization, maternity and newborn care, mental health and substance use disorder services, prescription drugs, rehabilitative and habilitative services and devices, laboratory services, preventive and wellness services and chronic disease management, and pediatric services, including oral and vision care. This comprehensive list ensures that critical medical needs are addressed, preventing individuals from being denied coverage for pre-existing conditions or facing exorbitant costs for necessary care.

The metal tiers—Bronze, Silver, Gold, and Platinum—indicate how your plan splits the cost of care with you. This split is often referred to as the plan’s actuarial value. A Bronze plan typically covers about 60% of your healthcare costs, leaving you responsible for the remaining 40%. Silver plans cover around 70%, Gold plans about 80%, and Platinum plans cover approximately 90%. While Platinum plans have the highest monthly premiums, they also offer the lowest out-of-pocket costs when you receive care. Conversely, Bronze plans have the lowest premiums but the highest out-of-pocket expenses.

Choosing the right metal tier depends on your anticipated healthcare needs and financial situation. If you expect to use a lot of medical services, a Gold or Platinum plan might be more cost-effective in the long run, despite higher premiums. If you anticipate minimal healthcare use, a Bronze plan might be suitable for lower monthly costs, provided you are prepared for higher out-of-pocket expenses if an unexpected health issue arises. Silver plans are particularly noteworthy because they are the only tier eligible for cost-sharing reductions, which can significantly increase their actuarial value for eligible individuals, making them a highly attractive option for many.

In 2026, the consistency of these essential health benefits across all Marketplace plans provides a baseline of quality care. The flexibility offered by the different metal tiers allows consumers to align their insurance choice with their budget and health expectations, ensuring that the ACA continues to fulfill its promise of accessible and comprehensive healthcare.

Future Outlook and Maximizing Your Benefits in 2026

The landscape of the Affordable Care Act is continuously evolving, with potential legislative changes and administrative adjustments influencing its provisions year by year. For 2026, while the core tenets of premium tax credits and subsidies are expected to remain, it’s prudent for consumers to stay informed about any new developments that could impact their eligibility or the generosity of financial assistance. Maximizing your ACA benefits requires a proactive approach, including careful planning and timely action.

Strategies for Optimal Coverage

One of the most effective strategies is to accurately estimate your household income for the upcoming year. Since subsidies are tied directly to income, a precise estimate helps the Marketplace calculate the correct amount of financial aid, preventing unpleasant surprises at tax time. If your income fluctuates, consider using a conservative estimate and updating it as your financial situation clarifies. Regularly reviewing your current plan and comparing it with other available options during the Open Enrollment Period is also vital. Plans and their associated costs can change annually, so what was the best option last year might not be the most suitable for 2026.

Engaging with the resources provided by the Health Insurance Marketplace can also significantly enhance your experience. Utilize the plan comparison tools, and don’t hesitate to seek assistance from trained navigators or certified brokers. These professionals can offer personalized guidance, help you understand complex terms, and assist with the enrollment process. They can also clarify how specific life events might qualify you for a Special Enrollment Period, ensuring you don’t miss out on crucial coverage.

Furthermore, understanding the difference between premium tax credits and cost-sharing reductions and how they apply to different metal-tier plans is paramount. For those eligible for CSRs, choosing a silver plan often provides the best value, combining lower premiums with reduced out-of-pocket costs. Being aware of the essential health benefits covered by all plans ensures you receive comprehensive care, from preventive services to prescription drugs. By combining accurate income reporting, diligent plan comparison, and leveraging available resources, you can effectively navigate the ACA in 2026 and secure the most beneficial health insurance for yourself and your family.

| Key Point | Brief Description |

|---|---|

| Premium Tax Credits | Financial assistance based on income to lower monthly health insurance premiums through the Marketplace. |

| Cost-Sharing Reductions (CSRs) | Subsidies that reduce out-of-pocket costs (deductibles, co-pays) for eligible individuals enrolled in Silver plans. |

| Income Impact | Changes in household income directly affect subsidy amounts; timely reporting to the Marketplace is crucial. |

| Essential Health Benefits | Ten categories of healthcare services that all Marketplace plans must cover, ensuring comprehensive care. |

Frequently Asked Questions About ACA 2026

Premium tax credits are government subsidies that lower your monthly health insurance payments. Eligibility in 2026 typically depends on your household income falling between 100% and 400% of the federal poverty level, and you must purchase a plan through the Health Insurance Marketplace. Recent legislative changes might expand these income thresholds.

Premium tax credits reduce your monthly insurance premiums, while cost-sharing reductions lower your out-of-pocket costs like deductibles, co-pays, and co-insurance when you receive medical care. CSRs are only available with silver-level plans for individuals with incomes below 250% of the federal poverty level.

It is crucial to report any income changes to the Health Insurance Marketplace as soon as possible. An income increase could reduce your subsidy, potentially leading to repayment at tax time. An income decrease could increase your subsidy, lowering your monthly premiums immediately and preventing under-subsidization.

All plans offered through the Health Insurance Marketplace in 2026 must cover ten categories of essential health benefits, including emergency services, hospitalization, prescription drugs, mental health services, and preventive care. This ensures comprehensive coverage, though specific services and cost-sharing can vary by plan and metal tier.

The exact dates for the 2026 Open Enrollment Period will be announced, but typically it runs from November 1st to January 15th of the following year. However, certain life events, like moving or losing other coverage, may qualify you for a Special Enrollment Period outside this window.

Conclusion

The Affordable Care Act continues to be a cornerstone of healthcare access in the United States, with its provisions for premium tax credits and subsidies playing a vital role in making health insurance attainable for millions. As we navigate 2026, understanding the mechanisms of financial assistance, the nuances of Marketplace enrollment, and the impact of personal circumstances on eligibility remains paramount. By staying informed, actively managing your enrollment details, and leveraging available resources, individuals and families can effectively utilize the ACA to secure comprehensive and affordable health insurance benefits, ensuring peace of mind and access to necessary medical care.